09 Mar The power of voluntary pension saving: Warren Buffett’s example at 10% annual returns

by Veronika Yordanova and Biser Ivanov

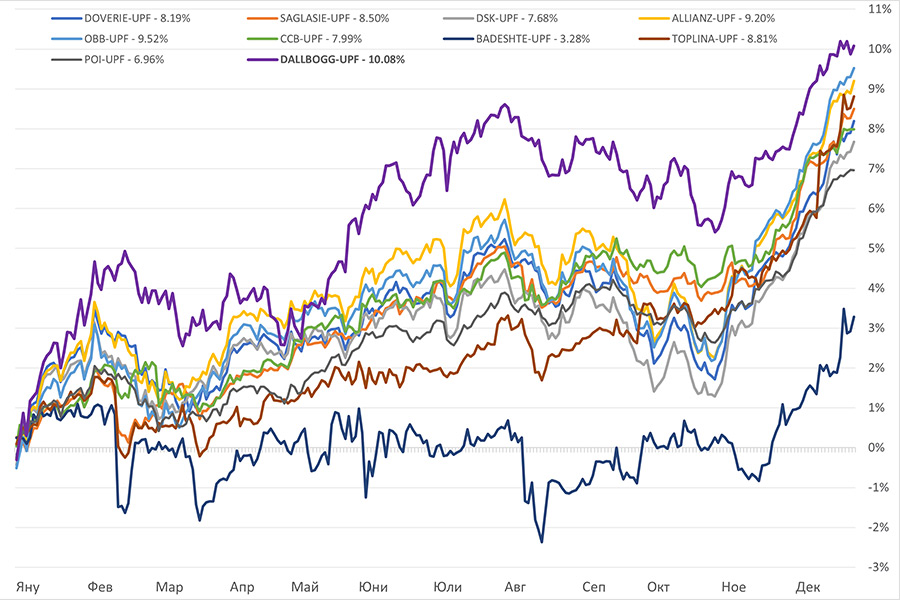

Investing in your future through retirement savings in a voluntary pension fund (VRF) is not only fashionable, but also very beneficial for personal finances and family security. High discipline and persistence in voluntary saving for retirement, from early or middle age, yields lasting results. Fund managers, within strictly regulated limits, are responsible for diversifying and balancing risk – with care to provide ever higher returns. We received thousands of questions, many positive comments and advice on the published annual return figures for universal pension funds in Bulgaria for 2023. Therefore:

- The results achieved in the relatively stable and safe, due to the extremely strict regulation, investment process speak for themselves:

- The award-winning American investor Warren Buffett, 93, also called the “Oracle of Omaha” because he lives in the state of Nebraska, defines successful investing as a snowball that we or our chosen stewards of our money – funds and others – roll down a snowy slope. If the slope is longer, i.e., if we start saving at an early age and live longer, even if the initial “snowball” is small, it will grow significantly at a 10% annual return. We will achieve the same result if we start with a larger ‘snowball’ in mid-life, again due to the same ‘compounding’ or ‘compound interest’ effect; in company growth there is a similar concept – Compound Annual Growth Rate, CAGR ). In other words, as a new 10% is added each year on top of the original investment, it also increases by 10% on the realised and compounded returns over the past years.

- Buffett’s example in dollars, which could be even more valuable in euros or euros at a 10% annual return if the depreciation of the dollar continues significantly longer:

10 thousand dollars invested today at a 10% annual compounded return will become almost 175 thousand dollars in 30 years, more than 450 thousand dollars in 40 years, and 1,170 million dollars in 50 years. The same extrapolation can be made for a 100 thousand initial investment in a voluntary pension fund over 30 years and a 10% annual compounded return, the amount could reach 1.750 million (i.e., 17.5 times or 17,500 percent increase); over 40 years, 4.5 million, and over 50 years the same amount, at the same annual return, could reach11.7 million!

Of course, all the examples and models are under the condition of actually achieved annual returns in a real maintained account (batch) with accumulation over the whole period.

______________________________ Special Reserve ____________________________