Recently, the Financial Supervision Commission published the final data on supplementary pension insurance activity for the first quarter of 2024. The results track the status and development of pension funds and investment returns, clearly outlining the pace of development of this important sector in Bulgaria’s economy.

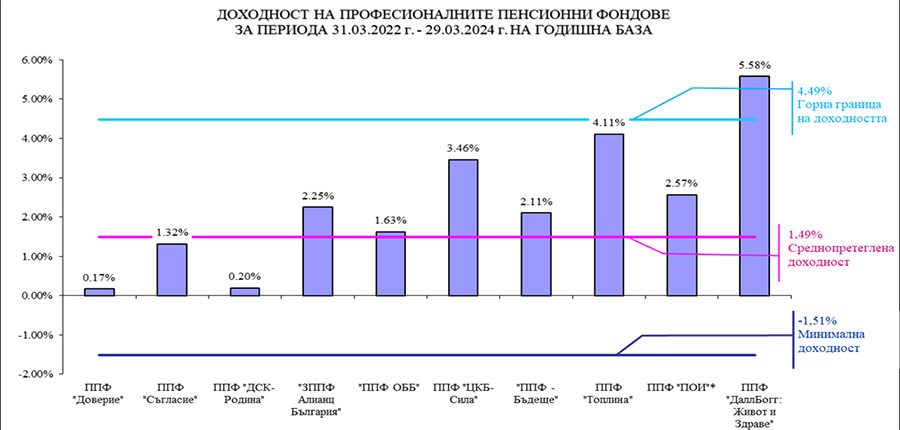

For the first reporting period, the last two years, the youngest pension insurance company, DallBogg Pensions: Life and Health, achieved a 5.58% return in its Occupational Pension Fund. The period encompassed the severe effects of the Covid-crisis as well as the devastating energy crisis, including two major wars, all of which impacted global product and financial markets. High inflation and high lending rates have also affected stock exchanges around the world in different ways. The volatility in the markets has caused uncertainty among investors, leading to considerable volatility in the prices of investment instruments and even indices such as the S&P 500, NASDAQ and Dow Jones have experienced large fluctuations. In response to increased inflation, interest rates have risen and remain predominantly at high levels worldwide, and many investors have shifted their capital away from equities towards lower-risk assets.

Amid this turmoil, the DallBogg Occupational Pension Fund not only managed to recover from a difficult 2022, but also to deliver a return of 9.49 per cent on its clients’ individual accounts at the end of 2023. For the period 31.03.2022 – 29.03.2024, the fund outperformed all other occupational pension funds in terms of returns, exceeding by 1.09% the maximum calculated by the FSC for those 24 months. Thus, the youngest Occupational Pension Fund in the country has set aside a reserve to serve as a future guarantee for the insured – this brings additional security for their pension investments.

Fear, panic and irrational decisions have led the way between 2022 and 2023, and only the most far-sighted and courageous have been able to overcome them in time to reap the rewards of their insight and hard work. DallBogg: Life and Health put in the effort and resources to adapt in time to the changing economic and geopolitical parameters. Through agile and expert management, the company has provided additional benefits to its insureds.

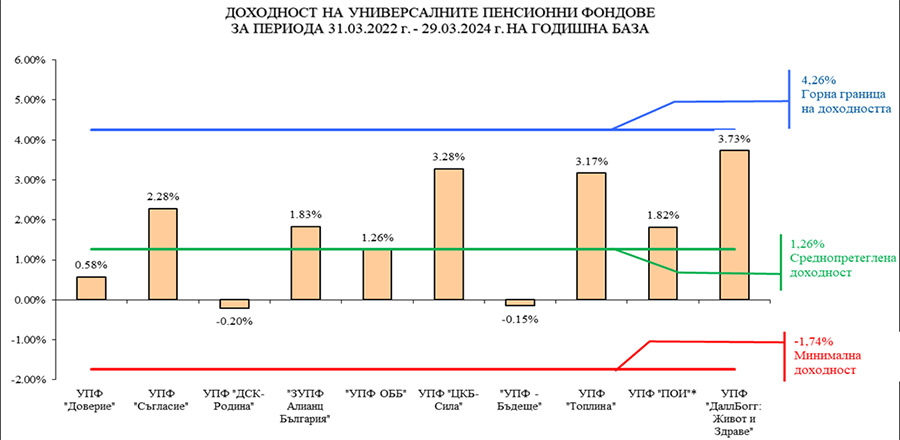

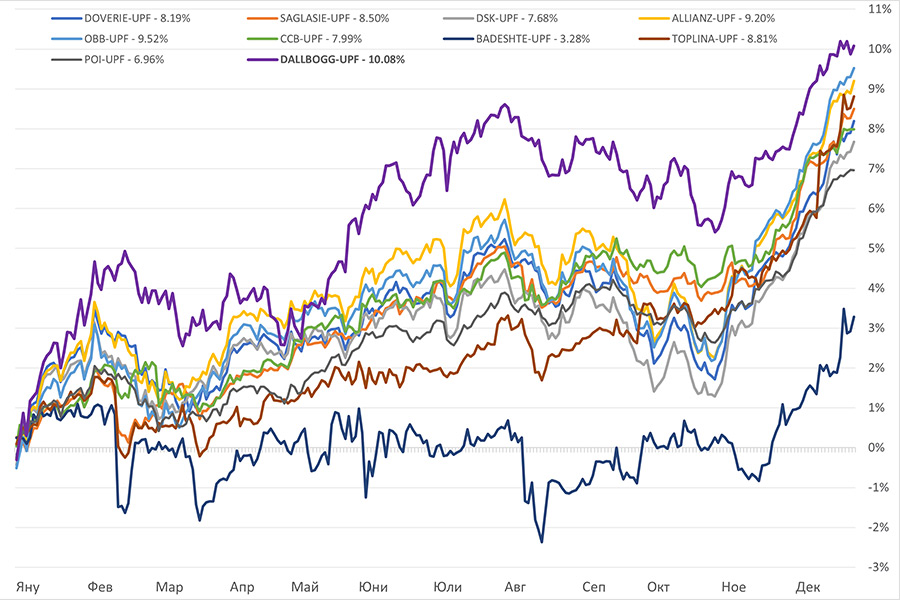

Financial experts also noted the success of the DallBogg: Life and Health Universal Pension Fund, which achieved an enviable return for 2023 and delivered a 10.08% increase in its customers’ account balances. For the period 31.03.2022 – 29.03.2024 it achieved a return of 3.73% and ranked ahead of all other universal funds.

For the mentioned 24-month period, the universal fund managed by “DallBogg: Life and Health” Pensions not only overcame the volatility of the financial markets, but also, through an adequate strategy and expert approach, managed to outperform the other nine funds of the same type (some with below-weighted average returns, others even with negative returns).

According to the FSC, when comparing the results of the supplementary mandatory pension insurance business for the first quarter of 2024 compared to the end of 2023, the growth rate of the two mandatory funds (PPF and UPF) managed by DallBogg: Life and Health Pensions is rapid and significant, which is an important indicator for measuring both the development of a company and the willingness of insured persons to change. For example, the number of clients and the amount of net assets in the DallBogg Ocupational Fund: Life and Health are increasing on a monthly basis, with the fund reporting an increase of 17.80% (vs. 0.44%average for the period for all professional funds) and 15.57% (vs. 3.66% average) respectively at the end of March 2024 compared to the end of 2023 figures. These performances significantly exceed those of the other nine occupational pension funds, while some of them even show a decline in the number of insured persons.

In the first three months of 2024, the number of insured persons in the DallBogg: Life and Health Universal Pension Fund increased by 14.99% (compared to an average of 0.58% for all universal funds over the period), and net assets increased by 15.21% (compared to an average of 4.72%). Within just one quarter, this growth is indicative of the high targets so far followed by expected results. And that’s not all. The data published by the FSC for the previous year is also interesting, and a careful review reveals that in all quarters of 2023. DallBogg: Life and Health Occupational and Universal Pension Fund are moving up on both indicators – number of insured persons and net assets. In one calendar year, clients in the professional fund increased by over 240% compared to December 2022, which is 120 times the average change for all professional funds in 2023. At the end of 2023, the net assets of the DallBogg: Life & Health Occupational Fund increased by over 250% compared to the end of 2022, which is more than 16 times the average change for the same funds over the period.

The performance of the DallBogg Occupational Fund: Life and Health in 2023, compared to the end of 2022, also outperforms all other universal funds and the numbers speak for themselves: the dynamics of the number of insured persons in the fund translates into an increase of 115%, which is more than 56 times the average change for all universal funds, and the change in net assets is close to 100%, i.e. almost 5 times the average increase over the period of funds of the same type.

Moving onwards and upwards has clearly been the main objective of POD DallBogg: Life and Health since the launch of its supplementary pension business. The remarkable performance of the company’s mandatory Occupational Fund and Universal Fund in the past 2023, in the first quarter of 2024, and for the past two-year period (31.03.2022 – 29.03.2024) has clearly highlighted the need for an alternative in the pension insurance market, which the youngest pension insurance company has provided to the Bulgarians.

Trends around the world and at home show that supplementary voluntary pension insurance is becoming an increasingly popular way to invest. All those who wish to receive professional service and have their funds managed by a motivated team with extensive experience in the financial sphere can contact the experts here.

___________________________ Special Reserve ____________________________

These results are not related to future performance and do not guarantee positive return. It is not guaranteed that the funds in the individual accounts at OPF „DallBogg: Life and Health“ will keep their full amount.

A description of the significance of the achieved rate of return and investment risk indicators

Nominal return – this is the return achieved on the management of a fund’s assets. It is calculated by dividing the difference between the value per unit of the fund valid for the last business day of the relevant year and the value per unit of the fund valid for the last business day of the previous year by the value per unit valid for the last business day of the previous year.

Standard Deviation – is a statistical measure of the dispersion of the values of a random quantity about its average or expected value. Standard deviation is accepted as one of the main indicators for measuring the risk of an investment portfolio.

Sharpe Ratio – an indicator that compares the returns achieved from managing an investment portfolio and the risk taken to achieve those returns.

The methodology for calculating the achieved nominal return and the level of investment risk is in accordance with Annex 15 of the „Regulation № 61/ 27.09.2018 of the FSC.

The investment policies of the funds managed by „PAC DallBogg: Life & Health“ are available on the Company’s website – https://dallbogg.bg, section „Investments“/ Rate of return and risk

A description of the significance of the achieved rate of return, the level of investment risk, the methodology for calculating and the investment policy of the fund are available on the Company’s website – https://dallbogg.bg, section „Investments“/ „Rate of return and risk“.

A comparison with the data can be made on the Financial Supervision Commission website (https://www.fsc.bg), section “Social Insurance activity”/ “Statistics”/ “Statistics and Analysis”/ 2023-2024